They keys of Fondviso: The disruptive public-private partnership model to promote affordable rental housing in Spain

In the first two articles, we contextualized the current housing access situation in Spain, the existing structural housing deficit, as well as the four needs of public administrations to be able to develop affordable social housing stock, taking into account the current public-private partnership models.

Now it’s time to talk about an effective solution to help public institutions and the private sector reduce the structural crisis and social vulnerability that exist in our country — in many cities that are already strained and in those that are starting to feel the strain — and improve the quality of life of families, young people, and the elderly who would like to access rental housing but find it impossible to do so.

Fondviso is the new infrastructure investment fund from Solventis that is socially responsible and the first of its kind in Spain. It is an innovative alternative for public management and private investment to expand the public affordable housing stock and reduce rental prices. Thanks to the characteristics of its public-private partnership, it reduces development costs and eliminates risks for private investment, all while avoiding public debt and housing subsidies. Fondviso therefore responds to the needs and interests of all the different stakeholders involved.

Fondviso is an innovative alternative for public management and private investment, to expand the stock of affordable public housing and reduce rental prices

For Solventis, Fondviso is more than an investment fund, it is an instrument for sustainable social transformation that invests in providing solutions for the population. For investors, it has the added value of being a socially responsible fund, a project with social impact, and of having an estimated net annual return of over 7%.

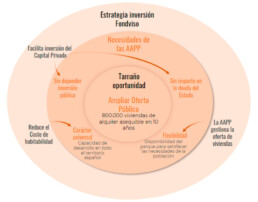

They keys to Fondviso’s investment strategy

At Solventis we have identified three levers that will drive the transformation of access to housing and the generation of long-term value in the Spanish residential segment, facilitating universal access to rental housing.

a) Housing as social infrastructure

This first lever develops the supply of affordable housing with an infrastructure model that specializes each stakeholder involved in the infrastructure development according to their long-term role. We distinguish three stakeholders, each with a specific functions: the landowner, which maintains ownership of the land and assigns the surface right to the investor; the investor, which is the owner of the infrastructure and responsible for investing in the development of the infrastructure/housing. The investor builds the infrastructure, obtains the ownership of the air rights, and cedes the right of use to the public operator. Finally, the third stakeholder is the public operator, which manages the rent with the renter and focuses on identifying the risks it wishes to assume based on the public housing policies being promoted at that time. In other words, the public operator is the owner of the use of the infrastructure and assumes the demand risk, the credit risk, the asset maintenance costs (managed by Fondviso subsidiaries), and the fee (94% of the rent) that the investor must pay (Fondviso investee companies) for the cession of the use of the infrastructure (housing).

The public operator covers the maintenance costs of the asset as well as the fee amount with 100% of the rent paid by the renters.

In short, this infrastructure model makes it possible to separate the roles of Investor and Operator of the infrastructure, making it possible to reduce infrastructure development costs, optimize the financial structure, eliminate intermediaries, create synergies through the industrialization of the infrastructure, and optimize the operational processes through standardization and digitalization.

b) Public-private partnership

The public-private partnership model proposed by Fondviso distributes the risks between public administrations and private capital, where the former are the public operators and assume the demand risk, and the private investor, as owner of the infrastructure, manages the development risk.

This risk distribution also makes it possible to reduce investor risk and optimize the resources of public administrations, thus achieving the main goal of reducing rental costs for renters, and more quickly boosting the public supply of affordable rental housing. In short, this new public-private partnership formula is an effective alternative for increasing the stock of affordable rental housing and relieving pressure on median incomes.

c) Sustainability

The Fondviso model is socially, environmentally ,and economically sustainable thanks to the distribution of responsibilities and benefits among all the stakeholders involved in managing and owning the infrastructure/housing. In the social orbit, it meets maximum environmental standards throughout the development process, such that the housing units reduce energy consumption by more than 40%, generate 95% of the energy they consume, and reduce water consumption by 30%. In other words, the model reduces maintenance and utility costs for renters. It is also worth noting that the Fondviso model fulfills 10 of the 17 Sustainable Development Goals set by the United Nations for the 2030 Agenda.

Economically, outsourcing the risks and omitting the cost of fees through the cession of public land to the Investor, among other attributes, makes it possible to estimate a target net return of over 7% (IRR). And in terms of social sustainability, the 30% reduction in habitability cost (we discuss this term further below) with the creation of more than 12,000 affordable housing units is a key step in ensuring the universal and equal right to housing in Spain. With the new model, the cession of use rights is key to being able to make housing and city planning policies according to the needs of municipalities, seeking the socio-economic integration of the housing stock.

Levers to reduce a home’s habitability cost

The Fondviso model is unique and disruptive in Spain because its investment approach directly impacts the habitability cost borne by renters. There are three attributes that can reduce a home’s habitability cost:

- New public-private partnership formula, focused on a pioneering distribution of risk between private capital and the public administration, that can reduce rents by eliminating the demand risk to the investor, which is assumed by the public administration.

- Housing as social infrastructure, where private investors reduce infrastructure investment costs by eliminating intermediaries in the value chain and optimizing resources through industrialization and standardization.

- Highly efficient assets, with high environmental sustainability of the housing aimed at enhancing energy efficiency and reducing CO2 emissions and water consumption. Therefore, the cost of habitability decreases as the consumption of supplies is reduced.

The Fondviso model is an alternative to the only two measures currently available today for public administrations and the private sector to expand the affordable housing stock: concessions and direct investments (which we covered in the article on public-private partnership opportunities in this blog). Unlike those, Fondviso is the only way to bring together the three central criteria for developing affordable social housing stock: universality, flexibility, and economic resources that don’t impact public resources or the national debt.

The opportunity for public-private partnership to improve access to housing in Spain

Now that we have explained the context of the housing access problem, it's time to talk about how it can be reversed or what solutions we can provide to address this structural crisis and social vulnerability affecting many strained capitals and cities, their surrounding areas that are starting to feel that strain, and even some of the more outlying towns and cities with a deficit in rental housing.

Thanks to the road map for public administrations that mandates the development of 800,000 affordable rental housing units in the next 10 years, a window of opportunity has opened for those bodies and private capital.

In this context, at Solventis we have analyzed four needs of public administrations in developing the public affordable housing supply, which we detail below. It must be universal, which is to say it must have development capacity throughout all of Spain and especially in those localities with a need for affordable housing stock. It must not fully depend on public investment or the availability of public resources. It must not impact the national debt. And it must be flexible, meaning that the housing stock must be able to adapt to the evolving needs of the town or the city in the long term, something that is only possible if the housing is managed by the Public Administration.

We have analyzed four needs of public administrations in developing the public affordable housing supply: dependence on public resources, impact on the national debt, universality, and flexibility

The private sector’s role in public-private partnerships

However, public administrations are not presently able to meet or cover all those needs, and they always have to forgo one or more of them. This is where the role of private capital can play a more significant role, with an opportunity to cover the needs of public administrations in expanding the public affordable housing supply.

What the private sector can do through public-private partnership:

- Attract or incentivize private capital on a grand scale and facilitate its investment, thus helping the public supply to not depend on public investment or impact the national debt.

- Reduce the habitability cost of housing below market price in a significant part of Spain — not just in the most strained cities — to impact at least 60% of the population, making the housing stock universal.

- Allow public administrations to manage the housing supply, or in other words, to be able to use the housing to apply the public housing policies considered necessary at any time based on demand needs. For instance, a public administration could facilitate young people’s access to housing during a short time or access for families during a longer time. To achieve this, it’s essential for the Public Administration to be able to select the segments of the population and set the terms of use for the housing units.

What happens with the current public-private partnership models?

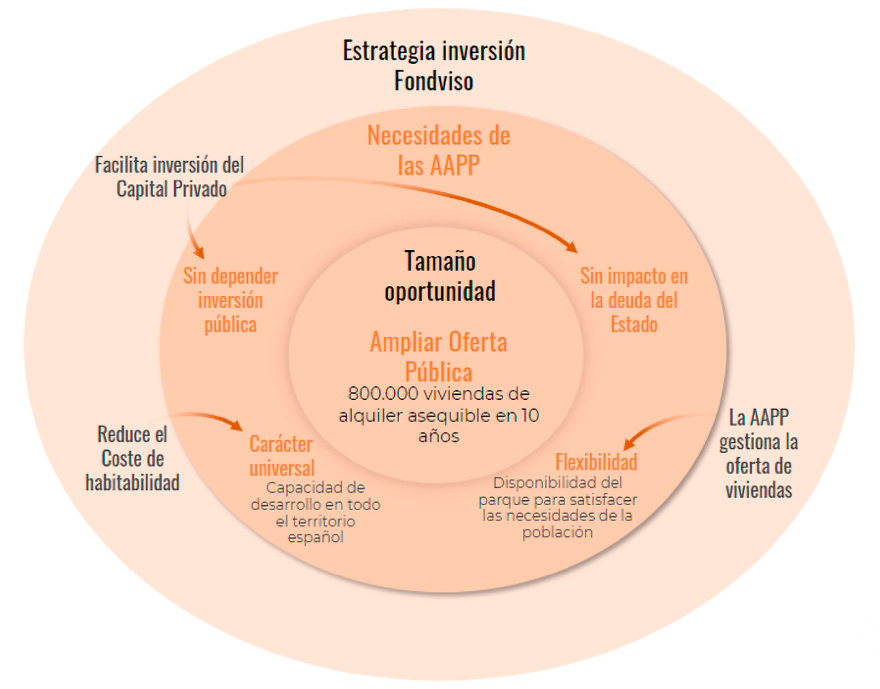

Public administrations currently have two major alternatives for increasing the supply of affordable rental housing: direct investment or establishing a public-private partnership model. Below we will describe the pros and cons of the models existing today, and whether or not they cover the four needs of public administrations.

1) Direct investment from public administrations

If the Public Administration makes a direct investment and operates the housing itself, taking on the demand risk and the maintenance cost, that does not cover two of the needs mentioned: the infrastructure development will depend on the availability of public resources; and it will also impact the national debt, meaning the development of this social structure will depend on the State’s borrowing capacity.

It would, however, cover the other two needs: universality, as the social infrastructure could be distributed wherever there is a need for housing access; and flexibility, because the housing stock could cover demand needs by the administration having total control to determine policies for selling or managing renters.

2) Public-private partnership based on a concession model

The other currently existing model is public-private partnership based on a concession model. In this case, it's the opposite needs that are covered: the infrastructure development will not depend on the availability of public resources, and therefore it will not impact the national debt.

However, the two needs of universality and flexibility remain unmet. In terms of universality, with the concession model, public administrations cede the land to the private sector for it to develop and then operate the housing, with private capital assuming both the development or construction risk (costs and time overruns), as well as the operating risk (operating costs), demand risk, and credit risk. Because it has to assume all the risk, the private sector strongly prefers areas with higher price strain, where there is less demand risk to be able to maintain above-average occupancy rates. These areas are also where the private sector can demand higher rent per useful square meter from the population, in order to more comfortably offset operational risks.

In terms of costs, it is becoming normal for the public administration to cede the lands to the private agent at no cost (without paying a fee), regardless of the legal form the deal takes (surface rights, for instance). This makes the housing development costs similar in different geographical areas.

On the other hand, the role of flexibility also goes unmet. The public administration does not assume risks or operating costs in exchange for not having the asset for the entire useful life of the concession, defining the asset's operating conditions at the outset. In other words, both the ownership and the use of the housing is in private hands, and the public administration loses the control to be able to define strategies and public policies to facilitate access to the housing based on the evolving needs of society or the population.

By following Fondviso’s public-private partnership investment strategy, a public administration would have control over the management of the public housing stock, and could therefore apply public policies to cover any needs unmet by the private sector. For example, it could use the public stock to prioritize housing access for a particular sector of the population, like young people. It could also use the affordable public stock to cover the income deficit experienced by a significant segment of the elderly population who own their homes, but lack the income to cover their needs for dependency services in a dignified way. Another example would be to support people having short-term economic struggles in a recession, considering that it's not the same to transfer subsidies or assistance to the private sector as it is to stop paying rent on housing owned by the public administration.

In conclusion, starting from the current scenario in which the public administration cannot assume the investment cost and the operating risk of the entire supply of affordable rental housing that needs to be developed, nor does it want to give up on having this housing supply distributed throughout the country (universality) and useful for all public administrations to cover the evolving population needs that may arise (flexibility), then public administrations need to be aware that they must remove some of the risks from the private sector.

The housing access problem in Spain

Access to housing in Spain is a years-old structural problem that can be explained by several economic and social factors latent in many areas of the country, confirming the idea that the current rental market is not meeting all the demand needs. That’s why ownership has a much greater weight in the Spanish real estate market.

At Solventis we want to provide some context to the housing access situation in Spain and describe the reasons behind this problem, as well as the solutions that we as experts in the field can offer.

Context and causes of the structural crisis

The context of the structural housing access problem in Spain is divided in two main circumstances. First, there is the structural housing deficit generated by a lack of sufficient development of Spain’s rental housing market, which is even worse in areas of the country that are particularly strained

According to Spain’s Affordable Housing Observatory, the affordable social housing in the country accounted for 2.5% of the total housing stock in 2019, significantly below the EU15 European average of 15% for the same year. The website also notes that only 2.8% of rents in Spain are below market price. So the country needs to build up this type of housing stock not only to reach European standards, but also to maintain its commitment to the state's Housing Act approved in May of 2023, which sets a target of increasing the proportion of social housing stock compared to the total number of homes by 20% in municipalities with strained areas in the next 20 years.

What are those strained areas of the country? The Big Data real estate platform Brainsre states that most of the strained areas are in Madrid, Barcelona, the Costa del Sol, the islands, and the Mediterranean coast, and include cities like Zaragoza, Valencia, Albacete, Ciudad Real, Cadiz, Huelva, and Murcia, among others. The new Housing Act considers a strained area to be any locality where the average burden of a mortgage payment or rent plus expenses is over 30% of the average income per household, or if the purchase or rental price has risen at least three points above the CPI in the five preceding years.

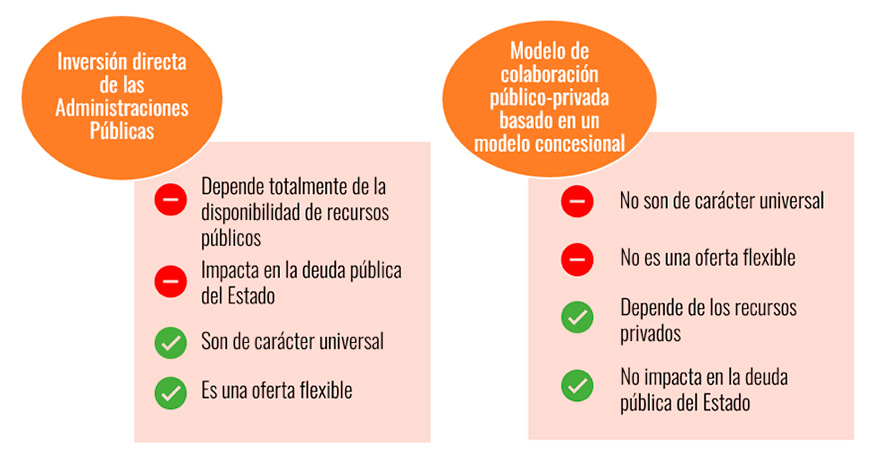

In terms of rental prices, according to the latest report from the website Idealista, the average monthly rental price in July of 2023 was 11.90 euros per built square meter, which means a monthly increase of 0.9%. Rental prices have gone up in 29 regional capitals, including: Barcelona, with the most expensive rent (€18.90/m2), Madrid (€17.10/m2), San Sebastian (€16.50/m2), Palma (€14/m2), Bilbao (€13.10/m2), and Malaga (€12.80/m2).

And therein lies the second factor behind the structural crisis in housing access: social vulnerability. The lack of access to affordable rental housing has a direct impact on a significant share of the population, especially families and young people.

According to Eurostat, 35% of families in Spain living in rented housing spend 40% of their income on rent, compared to the European Union average of 25%. Experts recommend that this percentage — known as the “effort rate” of purchasing or renting real estate — not go above 30%, which is to say a third of family income. The Idealista website’s study from the last quarter of 2022 lists seven capitals where the effort of renting a two-bedroom residence exceeds the recommended 30%: Barcelona requires the highest percentage of household income (39%), followed by Palma (35%), and Malaga (33%). Cities that are below the 33% include Madrid (31%), Valencia (31%), Alicante (31%), and San Sebastian (30%).

The lack of access to affordable rental housing has a direct impact on a significant share of the population, especially families and young people

Another problem is the situation among young people. The Fotocasa report “Young People and the Housing Market” from October of 2022 indicates that 52% of young people between 15 and 29 years old live in rental properties, because their economic situation prevents them from being able to purchase a home. In this sense, rental prices have a direct and absolute impact on their options for leaving home. According to Eurostat, Spanish youths leave home at 29.8 years old, three years later than the European average of 26.4 years old. Youth unemployment and the increase in rental prices in recent years are two of the clearest factors that make it difficult for young people to leave home and live independently, and therefore pursue a range of new opportunities in their lives.

In short, as indicated by Spain’s Affordable Housing Observatory, the country’s lack of affordable housing is due to several reasons, like high housing prices, constant increases in rents, the limited number of social and affordable housing units compared to the rest of Europe, and the need to spend a large portion of household income on housing. What solutions can we push forward to improve this situation among families and Spanish youth?

Possible solution: Expand the public rental housing stock

At Solventis our stated goal is to help increase the public supply of affordable social rental housing in Spain, in line with the road map set out by Public Administrations to develop 800,000 affordable social housing units in the next 10 years.

The Fondviso investment fund will respond to the needs of homes with net annual income of between 28,000 and 45,000 euros, which represent nearly 32% of the Spanish population.

It is a unique model that you can learn more about in our next blog posts, aimed at a large portion of society who until now has not had access to price-regulated housing but who suffers under the rising prices of the free market. This model will generate affordable housing throughout the country, both in the strained areas we mentioned and in other more outlying towns and cities that lack sufficient rental housing.