Now that we have explained the context of the housing access problem, it’s time to talk about how it can be reversed or what solutions we can provide to address this structural crisis and social vulnerability affecting many strained capitals and cities, their surrounding areas that are starting to feel that strain, and even some of the more outlying towns and cities with a deficit in rental housing.

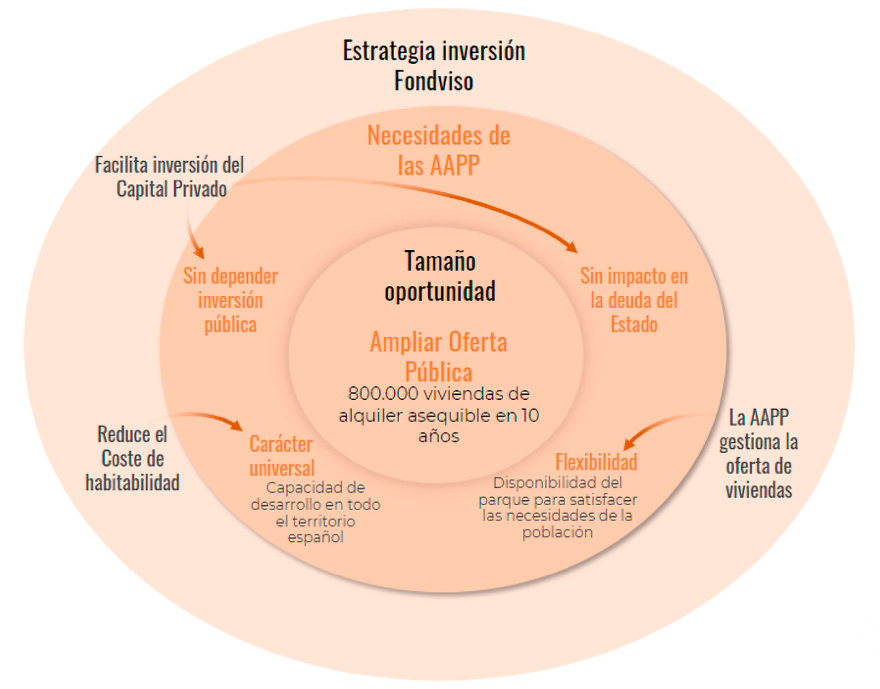

Thanks to the road map for public administrations that mandates the development of 800,000 affordable rental housing units in the next 10 years, a window of opportunity has opened for those bodies and private capital.

In this context, at Solventis we have analyzed four needs of public administrations in developing the public affordable housing supply, which we detail below. It must be universal, which is to say it must have development capacity throughout all of Spain and especially in those localities with a need for affordable housing stock. It must not fully depend on public investment or the availability of public resources. It must not impact the national debt. And it must be flexible, meaning that the housing stock must be able to adapt to the evolving needs of the town or the city in the long term, something that is only possible if the housing is managed by the Public Administration.

We have analyzed four needs of public administrations in developing the public affordable housing supply: dependence on public resources, impact on the national debt, universality, and flexibility

The private sector’s role in public-private partnerships

However, public administrations are not presently able to meet or cover all those needs, and they always have to forgo one or more of them. This is where the role of private capital can play a more significant role, with an opportunity to cover the needs of public administrations in expanding the public affordable housing supply.

What the private sector can do through public-private partnership:

- Attract or incentivize private capital on a grand scale and facilitate its investment, thus helping the public supply to not depend on public investment or impact the national debt.

- Reduce the habitability cost of housing below market price in a significant part of Spain — not just in the most strained cities — to impact at least 60% of the population, making the housing stock universal.

- Allow public administrations to manage the housing supply, or in other words, to be able to use the housing to apply the public housing policies considered necessary at any time based on demand needs. For instance, a public administration could facilitate young people’s access to housing during a short time or access for families during a longer time. To achieve this, it’s essential for the Public Administration to be able to select the segments of the population and set the terms of use for the housing units.

What happens with the current public-private partnership models?

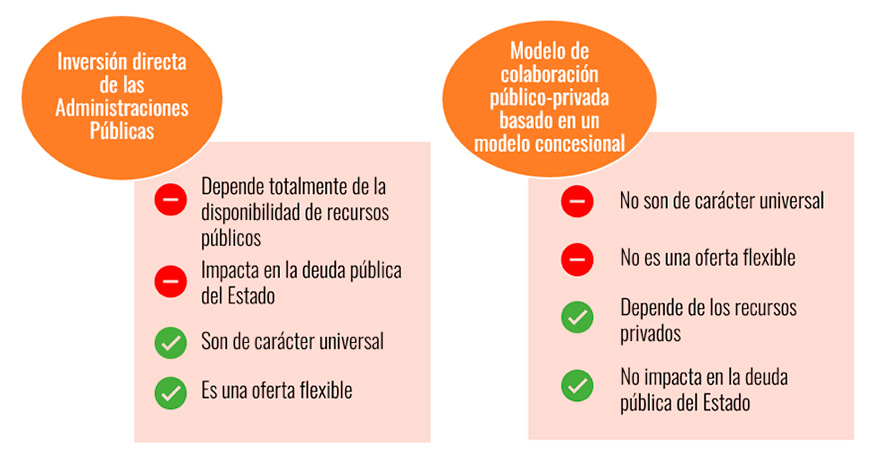

Public administrations currently have two major alternatives for increasing the supply of affordable rental housing: direct investment or establishing a public-private partnership model. Below we will describe the pros and cons of the models existing today, and whether or not they cover the four needs of public administrations.

1) Direct investment from public administrations

If the Public Administration makes a direct investment and operates the housing itself, taking on the demand risk and the maintenance cost, that does not cover two of the needs mentioned: the infrastructure development will depend on the availability of public resources; and it will also impact the national debt, meaning the development of this social structure will depend on the State’s borrowing capacity.

It would, however, cover the other two needs: universality, as the social infrastructure could be distributed wherever there is a need for housing access; and flexibility, because the housing stock could cover demand needs by the administration having total control to determine policies for selling or managing renters.

2) Public-private partnership based on a concession model

The other currently existing model is public-private partnership based on a concession model. In this case, it’s the opposite needs that are covered: the infrastructure development will not depend on the availability of public resources, and therefore it will not impact the national debt.

However, the two needs of universality and flexibility remain unmet. In terms of universality, with the concession model, public administrations cede the land to the private sector for it to develop and then operate the housing, with private capital assuming both the development or construction risk (costs and time overruns), as well as the operating risk (operating costs), demand risk, and credit risk. Because it has to assume all the risk, the private sector strongly prefers areas with higher price strain, where there is less demand risk to be able to maintain above-average occupancy rates. These areas are also where the private sector can demand higher rent per useful square meter from the population, in order to more comfortably offset operational risks.

In terms of costs, it is becoming normal for the public administration to cede the lands to the private agent at no cost (without paying a fee), regardless of the legal form the deal takes (surface rights, for instance). This makes the housing development costs similar in different geographical areas.

On the other hand, the role of flexibility also goes unmet. The public administration does not assume risks or operating costs in exchange for not having the asset for the entire useful life of the concession, defining the asset’s operating conditions at the outset. In other words, both the ownership and the use of the housing is in private hands, and the public administration loses the control to be able to define strategies and public policies to facilitate access to the housing based on the evolving needs of society or the population.

By following Fondviso’s public-private partnership investment strategy, a public administration would have control over the management of the public housing stock, and could therefore apply public policies to cover any needs unmet by the private sector. For example, it could use the public stock to prioritize housing access for a particular sector of the population, like young people. It could also use the affordable public stock to cover the income deficit experienced by a significant segment of the elderly population who own their homes, but lack the income to cover their needs for dependency services in a dignified way. Another example would be to support people having short-term economic struggles in a recession, considering that it’s not the same to transfer subsidies or assistance to the private sector as it is to stop paying rent on housing owned by the public administration.

In conclusion, starting from the current scenario in which the public administration cannot assume the investment cost and the operating risk of the entire supply of affordable rental housing that needs to be developed, nor does it want to give up on having this housing supply distributed throughout the country (universality) and useful for all public administrations to cover the evolving population needs that may arise (flexibility), then public administrations need to be aware that they must remove some of the risks from the private sector.